In the financial industry, risk is everything. Whether it be market risk, operational risk, representational risk, or credit risk, actors in financial markets base their decisions on measures of risk: calculations of potential losses and future events. Most risk today can be quantified to some degree – numerical indicators such as Value at Risk (VaR) allow financial analysts to simplify predictions and parse out precise degrees of probability. On the basis of these calculations, trades are made, companies are bought and sold, stocks are valued. Risk both defines and creates the market.

In the past forty years, the “theory of finance” has emerged as a veritable and independent academic discipline, merging economics with mathematics, statistics, and computer science in order to understand how financial markets work and how they can be made more effective. Since the early 1990s, new financial products and financial theories developed through the use of mathematics and computational finance have played an increasingly greater role in the financial industry. As Dr. Steven Shreve, Professor of Mathematics Carnegie Mellon University, writes, “finance has been modeled, computerized, and, in general, 'quantified.'” As a result, “the 'quants' who practice this kind of finance are slowly but surely moving into positions of power in investment banking, insurance, asset management, commodities trading, and regulation.”

I believe that this phenomenon has been largely under-investigated within anthropology and the larger public domain, particularly due to the esoteric nature of quantitative finance. What interests me is the way in which the quantification of finance is shaping the industry – culturally, ideologically, and structurally. How is finance being shaped by the growing number of “quants” that are entering the workforce? Who are these individuals, and what responsibility to they feel towards the scientific financial products that they are producing and implementing? In what ways does banking culture affect financial education, and what are the implications?

With regard to the "crisis," I hope to explore questions such as: how has the discipline of finance responded to the financial crisis (and resulting economic crises)? Has it at all? How has the “quantification” finance affected the industry's ability to react to and predict crises, and to what extent do students feel responsible for the long-term and social impacts of financial products that they help to develop and implement?

Projects:

Blogs:

Members:

Blog

{kind=link}

Finance and the City

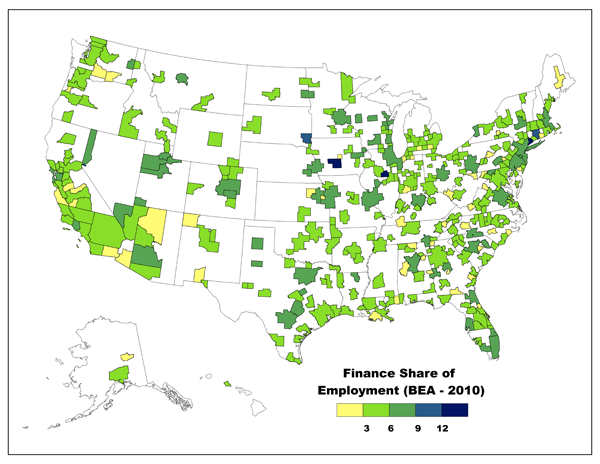

Richard Florida examines the new geography of finance within the United States. What about the role of finance in the geography of cities?

{kind=link}

Behind the noise: New York City

When I arrived in New York at the end of August to begin my field research on graduate programs in quantitative finance, I was struck by the overall level noise of the city. I knew that New York was loud – I had lived there for six years – but I had just how many individual sounds contribute to the the white noise of the city's streets.

{kind=link}